55th GST Council Meeting: Key Highlights and Implications

Dolphin Tanki 4.0: Empowering Young Entrepreneurs Across India

April 23, 2025

Legal Heir Not Liable for GST Dues Without Proof of Business Continuity: Jharkhand High Court

April 25, 2025

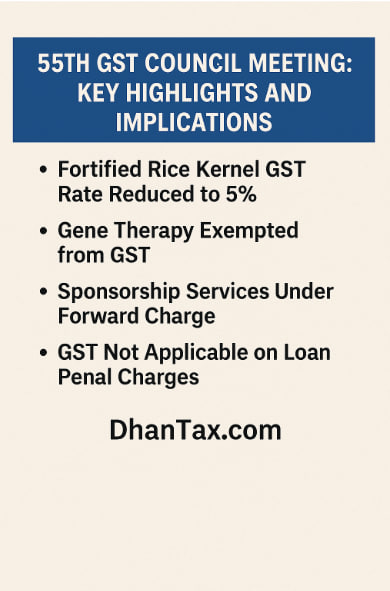

🧾 55th GST Council Meeting: Key Highlights and Implications

The 55th GST Council meeting, held on December 21, 2024, in Jaisalmer, Rajasthan, brought forth significant recommendations aimed at refining India’s GST framework.

📌 Major Recommendations:

Goods:

-

Fortified Rice Kernel (FRK): GST rate reduced to 5%.

-

Gene Therapy: Fully exempted from GST.

-

LRSAM Systems: Extended IGST exemption on assembly/manufacturing components.

-

Merchant Export Supplies: Compensation cess reduced to 0.1%.

-

IAEA Inspections: IGST exemption for specified equipment and samples.

-

Food Preparations for Free Distribution: Concessional 5% GST rate extended.

Services:

-

Sponsorship Services: Brought under Forward Charge Mechanism.

-

Motor Vehicle Accident Fund: Exemptions for contributions from third-party motor premiums.

-

Hotel Accommodation and Restaurant Services: GST rates tied to the preceding year’s supply value, effective April 1, 2025.

-

Composition Levy Scheme Rent: Reverse charge mechanism revised to exclude composition taxpayers.

Clarifications on Goods and Services:

-

Old and Used Vehicles: GST increased to 18%, applicable only on the supplier’s margin.

-

Autoclaved Aerated Concrete Blocks: GST clarified at 12%.

-

Agricultural Produce: Exemptions for green/dried pepper and raisins supplied by agriculturists.

-

Packaged Goods Definition: Revised to align with retail sales regulations.

-

Popcorn Classification: GST rates clarified for various types (5%, 12%, 18%).

-

RBI-Regulated Payment Aggregators: Eligible for GST exemption, excluding payment gateways.

-

Penal Charges: GST not applicable on penalties for loan non-compliance.

🔧 Trade Facilitation Measures:

-

Schedule III Amendment: Transactions in SEZ/FTWZs before clearance for export/domestic use are treated as neither goods nor services.

-

Voucher Taxability: Transactions in vouchers not treated as goods or services; distribution on a principal-to-agent basis remains taxable; no GST on unredeemed vouchers (“breakage”).

-

Input Tax Credit (ITC) Clarifications: ITC for goods delivered Ex-Works clarified as permissible.

-

Annual Return Late Fee Waiver: Partial waiver for delayed filings of FORM GSTR-9C (2017-18 to 2022-23), provided filing is completed by March 31, 2025.

⚙️ Compliance Streamlining:

-

Track and Trace Mechanism: Introduced via Section 148A of CGST Act, leveraging unique identification markings to prevent tax evasion.

-

Online Services Taxation: Supplier must record the recipient’s state for accurate GST application.

-

Pre-Deposit Amendments: Reduced pre-deposit requirement from 25% to 10% for appeals involving only penalties.

-

Temporary Identification Number (TIN): Introduced for non-registered entities making GST payments.

⚖️ Legal and Procedural Reforms:

-

Section 17(5)(d) Amendment: Retrospective replacement of “plant or machinery” with “plant and machinery” to clarify ITC eligibility.

-

Input Service Distributor (ISD) Reforms: Adjusted provisions to include interstate reverse charge mechanism (RCM).

-

Invoice Management System (IMS): Legal framework for generating GSTR-2B for improved compliance.

Stay Compliant with Dhan Tax

Navigating the evolving GST landscape can be complex. At Dhan Tax, we offer expert guidance to ensure your business remains compliant and optimized.

📞 Call us: +91 7678456921

🌐 Visit: www.dhantax.com